Section 529 college savings plans offer families a strategic vehicle to save for their children ‘s higher education expenses. Aimed to ease the financial burden of education, these plans provide opportunities for fund growth, flexibility in investment options, and tax benefits.

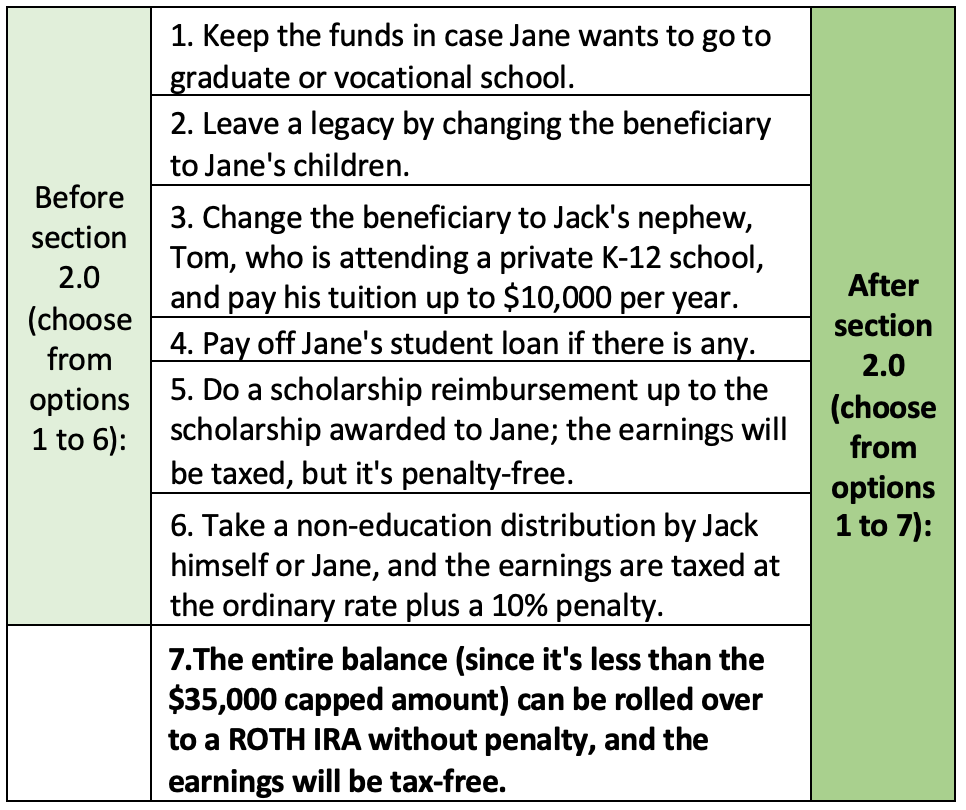

Sometimes, families may face another problem – they have saved too much money in a 529 college savings plan. In the past, options for addressing an overfunded 529 plan include:

- Keeping the fund in the account for advanced or continuing education.

- Changing the beneficiary to other children or a member of the extended family, such as niece, nephew or grandchildren.

- Making student loan payments.

- Making a penalty-free non-qualified withdrawal under some special cases, such as withdrawing up to the scholarship, however the earnings will still be taxed at the ordinary income tax rate.

- Taking a distribution, a 10 percent penalty will apply, and the earnings will still be taxed at the ordinary income tax rate.

Starting in 2024, thanks to the Secure Act 2.0, another option is introduced for transferring funds from a Section 529 college savings account to a Roth IRA for the same beneficiary without incurring federal income tax. This addresses the issue of excess funds in 529 accounts.

However, there are limitations: the total lifetime rollover limit is $35,000, and the 529 account must have been active for at least 15 years.

Annual rollover amounts are capped at the IRA contribution limit for the given year (e.g., $6,500 for individuals under 50 in 2023). Moreover, the rollover cannot surpass the beneficiary's earned income for the year, and contributions and earnings from the preceding 5 years cannot be rolled over.

For example, Jack has been funding a 529 account for his only daughter, Jane, for the past 19 years. After Jane graduated from college, Jack's choices about the remaining $34,000 in the account are...

As the cost of higher education continues to rise, the 529 college savings plan emerges as a vital tool for families to proactively prepare for their children's educational journey, ensuring a smoother transition into academic pursuits without overwhelming financial strain. From Jack’s case, this change presents a significant tax planning opportunity for beneficiaries with surplus funds in their 529 accounts.

In the meantime, both the IRS and individual states may provide further guidance. For instance, it remains uncertain whether changing beneficiaries resets the 15-year waiting period before a rollover, or if individual states will align with federal law to permit tax and penalty-free rollovers.

For further clarification, it is recommended to seek advice from a financial or tax professional to ensure accuracy and compliance with relevant laws and regulations.